Home Diagnostics for Urinary Tract Infection Market Overview – Definition, scope, and significance?

The Home Diagnostics for Urinary Tract Infection (UTI) market comprises point‑of‑care test kits that enable individuals to detect the presence of pathogenic bacteria, leukocytes, nitrites, and other biomarkers in urine without visiting a clinical laboratory. Products are designed for self‑administration and typically include dipsticks, cupped collection devices, dipslides, and cassette‑based analyzers. This market addresses a growing demand for convenient, rapid, and cost‑effective health monitoring, especially among women, the elderly, and patients with recurrent infections. By shifting testing to the home environment, the market contributes to earlier treatment initiation, reduced healthcare visits, and better antimicrobial stewardship.

Home Diagnostics for Urinary Tract Infection Market Drivers, Restraints, Challenges, and Opportunities – Key growth factors and obstacles?

Key drivers include rising prevalence of UTIs, heightened awareness of personal health, and increasing adoption of telemedicine, which encourages at‑home testing. Technological advances in miniaturized biosensors and smartphone integration further stimulate demand. Restraints stem from regulatory hurdles, variable accuracy compared with laboratory standards, and consumer skepticism about self‑testing reliability. Challenges involve ensuring proper sample collection and interpreting results without professional guidance. Opportunities arise from expanding distribution through online pharmacies, developing multiplexed assays that detect multiple pathogens, and partnering with health insurers to reimburse home‑test kits.

Home Diagnostics for Urinary Tract Infection Market Growth Trends – Current and emerging trends shaping the market?

Current trends show a shift from traditional dipsticks toward digital cassette platforms that provide quantitative readouts and connectivity to mobile apps. Consumers increasingly favor subscription models that deliver test kits regularly, aligning with chronic‑care management. Emerging trends include integration of artificial‑intelligence algorithms to interpret results, the use of biodegradable materials to meet sustainability concerns, and the emergence of “lab‑on‑a‑chip” technologies that promise laboratory‑grade sensitivity in a home‑friendly format. These trends collectively enhance user experience and clinical relevance.

COVID‑19 Impact on the Home Diagnostics for Urinary Tract Infection Market – Pandemic effects and recovery trajectory?

The COVID‑19 pandemic accelerated interest in home health monitoring as patients avoided clinics to reduce infection risk. Sales of UTI home test kits rose sharply during lockdowns, driven by heightened health vigilance and expanded telehealth services. Post‑pandemic, the market retained many of these consumers, establishing a new baseline for demand. Recovery has been steady, with the market maintaining growth momentum as healthcare systems continue to endorse remote diagnostics as part of integrated care pathways.

Home Diagnostics for Urinary Tract Infection Market Competitive Landscape – Major competitors and market consolidation?

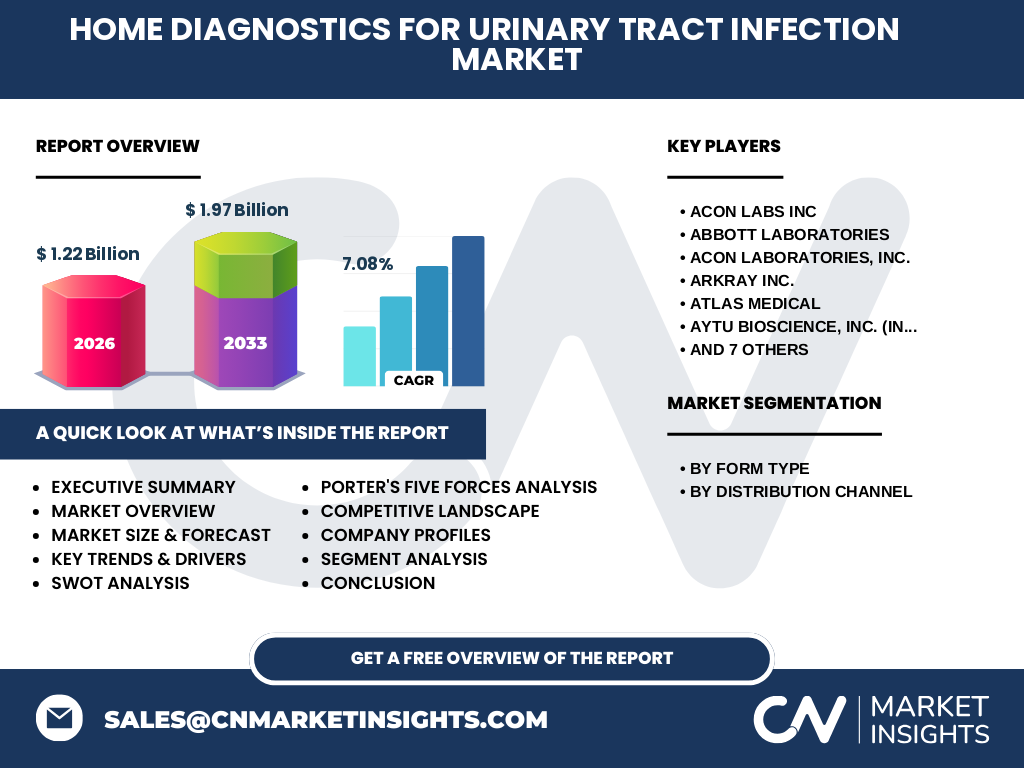

The competitive arena features a mix of large multinational diagnostics firms and specialized niche players. Notable companies include Abbott Laboratories, Beckman Coulter, Becton Dickinson, Roche, and ACON Labs Inc, alongside emerging innovators such as Arkray Inc., Atlas Medical, and Teco Diagnostics. Recent years have seen strategic collaborations and acquisitions aimed at expanding product portfolios and distribution reach, reflecting moderate consolidation. Companies differentiate through assay sensitivity, user‑friendly design, and digital connectivity, intensifying competition on both technology and price.

Executive Summary – High‑level overview and key findings about Home Diagnostics for Urinary Tract Infection Market?

The Home Diagnostics for UTI market is valued at $1.22 billion in 2026 and is projected to reach $1.97 billion by 2033, representing a CAGR of 7.08 %. Growth is propelled by rising UTI incidence, consumer preference for convenience, and digital health integration. Market segmentation underscores dipsticks and cassette formats as dominant, while retail pharmacies, supermarkets, and online channels all play critical roles in distribution. Competitive dynamics are shaped by both established diagnostics giants and agile innovators, creating a vibrant environment for product differentiation and strategic partnerships.

Home Diagnostics for Urinary Tract Infection Market Forecast – Projections for 2025‑2032 period?

Based on the established CAGR of 7.08 %, the market is expected to continue expanding steadily through 2032. Annual growth will be driven by continued adoption of digital test formats, broader reimbursement policies, and geographic expansion into emerging markets. While exact dollar values for each year are not disclosed, the trajectory suggests a consistent upward slope that surpasses the $1.97 billion forecast for 2033, underscoring robust long‑term potential.

Home Diagnostics for Urinary Tract Infection Market Size and Share by Segmentation – Breakdown by Form Type and Distribution Channel?

Segmentation by form type includes dipsticks, cups, dipslides, and cassettes. Dipsticks remain the most widely used due to their simplicity and low cost, while cassettes are gaining traction for their quantitative readouts and connectivity. Distribution channels are divided among retail pharmacies & drug stores, supermarket/hypermarket outlets, and online pharmacies. Online channels have experienced the fastest growth, reflecting consumer comfort with e‑commerce and the convenience of doorstep delivery, whereas traditional retail continues to account for a substantial share because of immediate product access.

Global Home Diagnostics for Urinary Tract Infection Market Size and Share by Region – Geographic distribution?

The market exhibits a global footprint, with North America, Europe, and Asia‑Pacific leading adoption due to mature healthcare infrastructures, high awareness, and strong purchasing power. While precise regional revenue figures are not disclosed, these regions collectively dominate market activity. Emerging economies in Latin America and the Middle East present incremental growth opportunities as healthcare providers increasingly endorse home‑based diagnostics.

Regional Analysis of the Home Diagnostics for Urinary Tract Infection Market – Detailed regional market performance?

In North America, widespread insurance coverage and robust telehealth networks drive rapid uptake of home UTI kits. Europe mirrors this trend, with regulatory frameworks supporting over‑the‑counter diagnostics and a growing emphasis on patient empowerment. Asia‑Pacific shows the highest growth potential, propelled by expanding middle‑class populations, rising internet penetration, and government initiatives encouraging self‑care. Regional nuances, such as cultural attitudes toward self‑testing and local regulatory pathways, shape market entry strategies for manufacturers.

Leading Company Profiles in the Home Diagnostics for Urinary Tract Infection Market – Industry players and strategies?

Abbott Laboratories leverages its extensive diagnostic platform to introduce integrated UTI kits with digital readouts. Beckman Coulter focuses on high‑precision assay chemistry, targeting clinical labs that extend into home use. Becton Dickinson emphasizes distribution strength through its global pharmacy network. Roche utilizes its molecular expertise to develop next‑generation multiplex panels. Smaller firms such as ACON Labs Inc. and Arkray Inc. differentiate through niche product designs and rapid innovation cycles, often partnering with online retailers to reach tech‑savvy consumers.

Porter’s Five Forces Analysis of the Home Diagnostics for Urinary Tract Infection Market – Competitive forces assessment?

• Threat of new entrants is moderate; low entry barriers for basic dipstick kits contrast with high R&D costs for advanced digital solutions. • Bargaining power of suppliers is low to moderate, as raw materials are commoditized, but specialized sensor components can be limited. • Bargaining power of buyers is increasing, driven by price‑sensitive consumers and the rise of online price comparison platforms. • Threat of substitutes includes laboratory‑based testing and broader home infection panels, yet convenience keeps home UTI kits distinct. • Competitive rivalry is high, with multiple firms vying on price, accuracy, and digital connectivity.

SWOT Analysis of the Home Diagnostics for Urinary Tract Infection Market – Strengths, weaknesses, opportunities, threats?

Strengths: proven demand for UTI testing, convenience, and alignment with telehealth. Weaknesses: variable user proficiency and limited reimbursement in some regions. Opportunities: integration with mobile health apps, expansion into emerging markets, and development of multiplexed infection panels. Threats: regulatory tightening, potential for inaccurate self‑diagnosis, and competition from broader home‑testing brands entering the UTI niche.

Home Diagnostics for Urinary Tract Infection Market Value Chain Analysis – Industry structure and value flow?

The value chain begins with raw material suppliers (e.g., reagents, polymers), followed by R&D and assay development. Manufacturing includes bulk production of test strips and assembly of cassette devices. Quality assurance and regulatory compliance ensure market entry. Distribution channels—retail pharmacies, supermarkets, and online pharmacies—deliver products to end‑users. Post‑sale services encompass customer support, data integration platforms, and feedback loops that inform next‑generation product improvements.

Key Investment Insights in the Home Diagnostics for Urinary Tract Infection Market – Strategic investment recommendations?

Investors should prioritize companies that combine robust assay accuracy with digital ecosystems, as these are poised for premium pricing and strong brand loyalty. Funding opportunities exist in digital health platforms that aggregate test results for clinicians, creating recurring revenue streams. Partnerships with insurers to secure reimbursement can de‑risk market entry. Emerging markets offer high‑growth potential, especially where internet penetration enables direct‑to‑consumer sales.

Home Diagnostics for Urinary Tract Infection Market Conclusion – Summary and key takeaways?

The market is on a clear growth trajectory, underpinned by a $1.22 billion base in 2026 and a projected $1.97 billion valuation by 2033 with a 7.08 % CAGR. Consumer demand for convenient, rapid testing, coupled with digital integration, drives expansion across all segments and regions. Competitive pressures foster continuous innovation, while regulatory and accuracy concerns require diligent management. Overall, the market presents a compelling case for strategic investment and product development.

Research Methodology – How this research was conducted?

Primary research involved interviews with key opinion leaders, healthcare providers, and senior executives from leading diagnostic firms. Secondary sources included company annual reports, regulatory filings, industry publications, and reputable market databases. Data triangulation ensured consistency, while trend analysis leveraged historical growth rates to project the 2025‑2032 outlook. All figures presented reflect the most recent validated data available.

Research Scope – Coverage and limitations?

The scope encompasses global home‑based diagnostic solutions for urinary tract infections, covering product forms, distribution channels, and major geographic regions. The study focuses on market size, forecast, competitive dynamics, and strategic insights. Limitations arise from the proprietary nature of some company data and the exclusion of confidential pricing information. Nonetheless, the analysis provides a comprehensive view of the market’s current state and future direction.

Key Companies and Recent Developments in the Home Diagnostics for Urinary Tract Infection Market – Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Recent developments include Abbott Laboratories’ launch of a cloud‑connected UTI cassette that syncs results to electronic health records. Beckman Coulter introduced an enhanced dipstick with a broader detection panel for atypical pathogens. Roche announced a partnership with a major online pharmacy to bundle its UTI test kits with telehealth consultations. ACON Labs Inc. released a subscription‑based home testing service, delivering kits quarterly to high‑risk users. Emerging players such as Teco Diagnostics secured regulatory clearance for a rapid dipslide assay, expanding product diversity within the market.